A good Power Purchase Agreement (PPA) and understanding of operating costs is even more essential for natural gas CHP after the Capacity Market (CM) auction cleared at it’s lowest ever rates this month.

There were two auctions:

T-1 for Oct18-Sept19

- Cleared at £6.00/kW

- Previous low £6.95/kW

T-4 for Oct21-Sept22

- Cleared at £8.40/kW

- Previous low £18.00/kW

Both results were below even the most pessimistic expectations. Especially when we consider the impact of:

- Reducing TRIAD income for embedded generators

- The Medium Combustion Plant Directive restricting diesel generators

- Low de-rating factors for batteries.

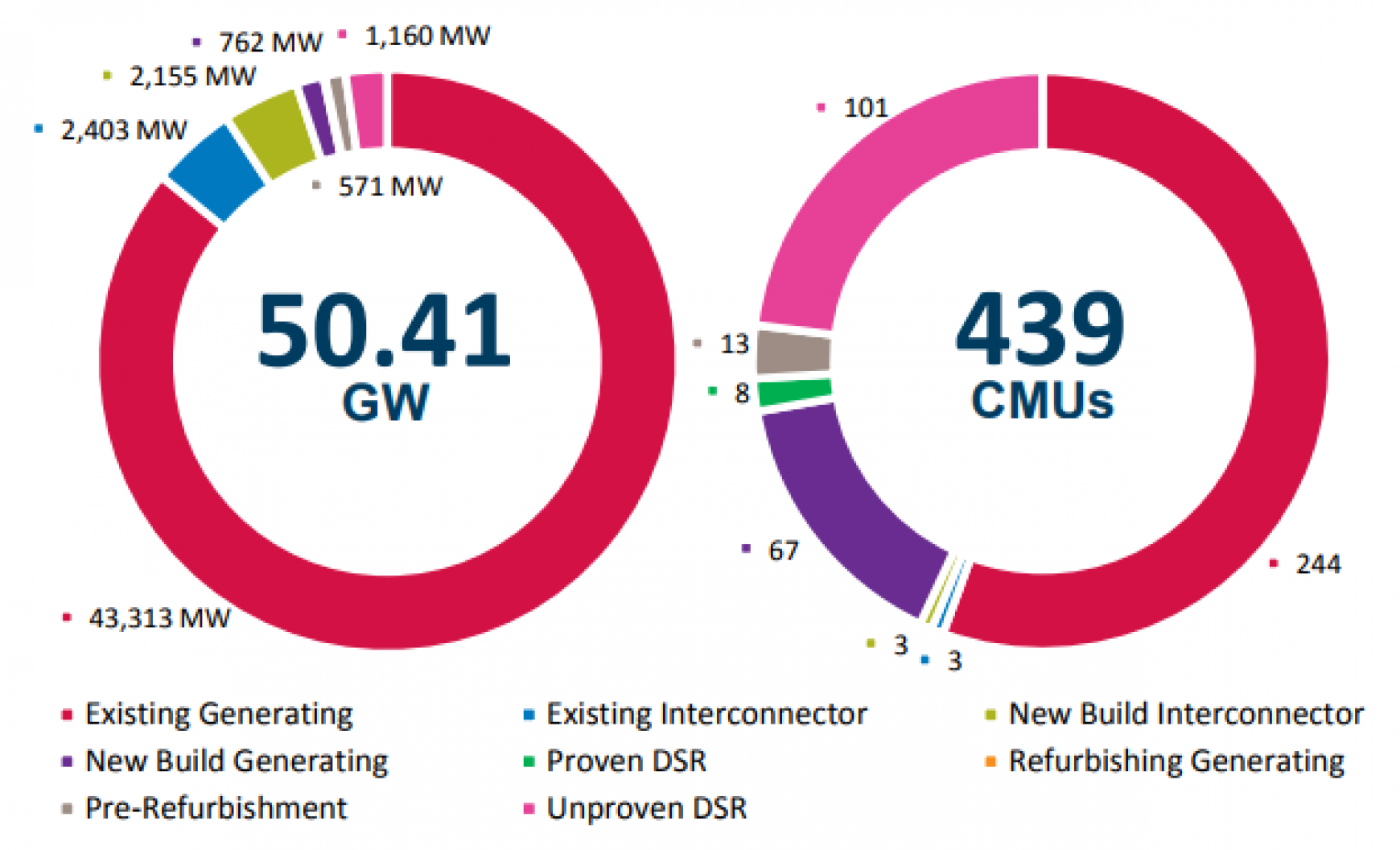

No doubt the coming days will see all sorts of analysis about how/why this happened. But it seems that there is simply plenty of generation capacity on the ground now that is still expecting to be running in 4 years time whether they earn CM income or not. Of the 50GW required, 90% came from existing generation & interconnectors. And to think that the CM was created because a shortage was expected. But, maybe this is just the prolonged lull before the ‘Capacity Crunch’ storm finally hits. After all, coal fuelled power stations are closing at such a rate the government target of none by 2025 is likely to be delivered early the market alone and the CM has been so low that little in the way of significant new generation has been built.

Image courtesy of http://bit.ly/2BkPJbR